Table of Content

Escrow is a legal arrangement where a third party temporarily holds money on behalf of a buyer and seller in a real estate transaction. Once you have a loan, you pay it back in small increments every month over the span of years or even decades. It’s essentially a long, life-changing IOU that helps many Americans bring the dream of homeownership within reach.

Message and data rates may apply from your service provider. Want to learn more about mortgages, refinancing and home equity? Our mortgage dictionary covers a variety of terms, and our FAQs provide answers to common buying and homeownership questions. With our affordability calculator you can see how much you may be able to afford based on different scenarios, like how much you put down or the length of your loan.

How to lower your monthly mortgage payment

Most modern lenders allow you to set up a direct debit to your bank account, typically on a scheduled day of the month. This allows you some control, without risking errors. Automatic billing is excellent when you have stable income.

Since the conventional DTI ratio maximum is 45% to 50%, you likely can afford this payment. Escrow is a service that holds money between a transfer of goods from one person to another. Neither side knows the other, so neither trusts the other.

Making the Offer

Sample payments include principal and interest only. This mortgage payment calculator assumes that you have a 20% down payment, unless you specify otherwise. If you have less than a 20% down payment, you may have to pay private mortgage insurance , which would increase your monthly mortgage payment. If you opt for ARMs, your mortgage interest rates will change over time.

If you're not careful, you get stuck with the bill. Most of the time, lenders will not allow an inspection prior to purchase of a foreclosed home. You are, more or less, gambling on the quality of the home.

Conforming loans vs non-conforming loans

But what if you’re self employed, or have 1099 income? It can be more challenging to apply for those types of loans withuneven income. TPH ZeroDown Brokerage Inc can help with a few different, non-traditional options and we often work with self-employed individuals to help them get financing. Find more details here and begin the process today. Fine-tune your inputs to assess your readiness.

As a homeowner, you’ll pay property tax either twice a year or as part of your monthly home payment. This tax is a percentage of a home’s assessed value and varies by area. For example, a $500,000 home in San Francisco, taxed at a rate of 1.159%, translates to a payment of $5,795 annually. 30-year fixed-rate mortgage - The most common option, typically has a lower monthly payment and your payment doesn't change. Purchase price refers to the total amount you agree to pay to the property’s seller. This amount is typically different from your loan amount, since most lenders won’t loan you the full amount of a property’s purchase price.

Determining what your monthly house payment will be is an important part of figuring out how much house you can afford. That monthly payment is likely to be the biggest part of your cost of living. It is the amount of equity; you pay at the time of purchase. For example, if you buy a house for $300,000 and pay $15,000 initially, your down payment is 5%.

Principal, interest, taxes and insurance are the building blocks of a mortgage payment and a few of the common mortgage terms you’ll find on the homebuying journey. Interest is what the lender charges for borrowing money and varies depending on the market and candidate. A mortgage should be between about 20 to 25 percent of your gross income.

A higher down payment is enticing to lenders and can help get you approved. Putting less down is cheaper upfront, but you need to do some convincing to get it. Additionally, if you are paying under 20 percent, you will be required to get Private Mortgage Insurance. PMI is a type of insurance specifically designed to compensate the lender if you default while having paid a lower-than-usual down payment.

Credit report fees are relatively minor, typically less than $100. This is simply a way for the lender to obtain a current copy of your credit report. Make sure you've pulled it yourself before you waste your time -- and the lender's time -- with a low score or problematic report. You'll lose your fees and you'll end up declined. While that stability can be quite beneficial, these often have higher starting rates than adjustable loans.

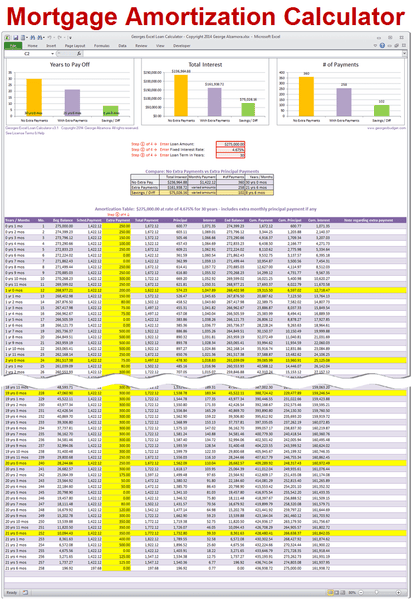

These rates are usually given in annual terms and mostly remain unchanged for the life of a loan that we will discuss in detail later in the loan type section. This mortgage calculator considers all these costs (and more!) and will optionally include them in a mortgage payment schedule. The more you put down, the lower your mortgage payment will be. If you make less than a 20% down payment, the calculator will estimate how much private mortgage insurance you might pay . Use our mortgage calculator to calculate monthly payment along with Taxes, Insurance, PMI, HOA & Extra Payments on your home mortgage loan in the U.S.

Your estimated annual property tax is based on the home purchase price. The total is divided by 12 months and applied to each monthly mortgage payment. If you know the specific amount of taxes, add as an annual total. For the Adjustable-Rate Mortgage product, interest is fixed for a set period of time, and adjusts periodically thereafter.

No comments:

Post a Comment